Defining a “Good” Rate of Return on Investments

What is a good rate of return on investments – Determining a satisfactory rate of return on investments is subjective and depends heavily on individual circumstances. Several factors influence what constitutes a “good” return for a specific investor.

Factors Influencing Return Perception

An investor’s risk tolerance, time horizon, financial goals, and available investment options all play a crucial role in shaping their expectations. A higher risk tolerance often correlates with a desire for higher returns, while a longer time horizon allows for greater potential for growth.

Investor Profiles and Return Expectations

| Investor Profile | Risk Tolerance | Return Expectation |

|---|---|---|

| Conservative Investor | Low | Low to moderate (e.g., 3-5% annually) |

| Moderate Investor | Medium | Moderate to high (e.g., 6-10% annually) |

| Aggressive Investor | High | High (e.g., 10%+ annually) |

Risk Tolerance and Acceptable Return Rates

Higher risk generally implies the potential for higher returns, but also carries a greater chance of losses. Conservative investors prioritize capital preservation and accept lower returns, while aggressive investors are willing to take on more risk for potentially higher gains.

Historical Average Returns of Various Asset Classes

| Asset Class | Average Annual Return (Historical, approximate) | Risk Level |

|---|---|---|

| US Treasury Bonds | 5-7% | Low |

| Corporate Bonds | 6-9% | Medium |

| Stocks (US Equities) | 10-12% | High |

| Real Estate | 6-8% | Medium |

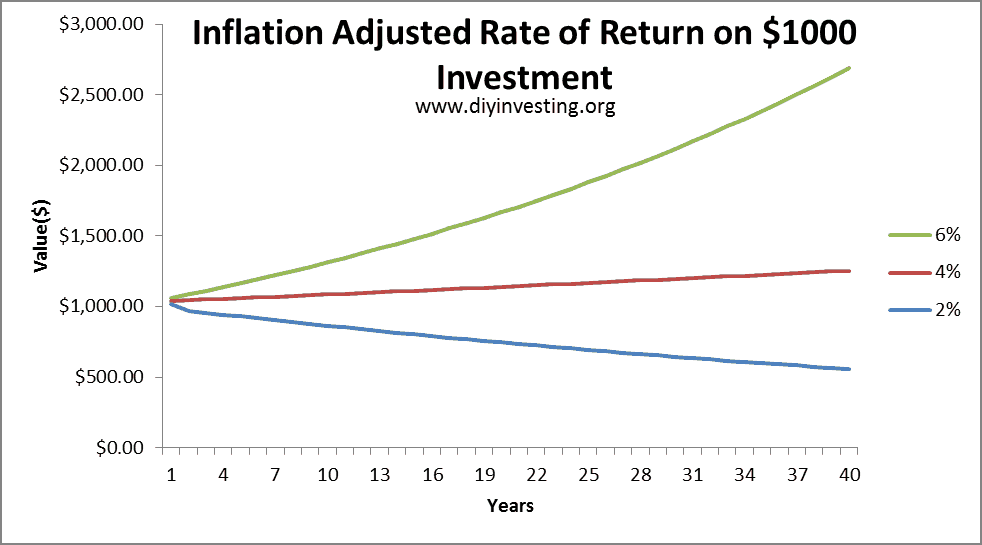

Inflation’s Impact on Returns

Inflation erodes the purchasing power of money over time. Understanding its impact is crucial for assessing the true return on investments.

Inflation and Purchasing Power

Inflation reduces the value of future cash flows, meaning that a nominal return of 10% might only represent a real return of 5% if inflation is 5%. This is because the same amount of money buys less after inflation increases prices.

Calculating Real Rate of Return

The real rate of return is calculated by adjusting the nominal return for inflation. The formula is: Real Rate of Return = [(1 + Nominal Rate) / (1 + Inflation Rate)] – 1

Historical Inflation and Investment Returns

| Year | Inflation Rate (Example) | Nominal Return (Example) | Real Return |

|---|---|---|---|

| 2022 | 7% | 10% | 2.8% |

| 2023 | 3% | 8% | 4.9% |

Nominal vs. Real Returns

Nominal returns represent the raw percentage change in investment value, while real returns reflect the increase in purchasing power after accounting for inflation.

Risk and Return Relationship

Investment returns are intrinsically linked to risk. Higher potential returns typically come with higher risk.

Types of Investment Risks

- Market Risk: Fluctuations in overall market conditions.

- Interest Rate Risk: Changes in interest rates affecting bond prices.

- Inflation Risk: Erosion of purchasing power due to inflation.

- Credit Risk: The risk of a borrower defaulting on a loan.

Risk-Return Profiles of Asset Classes

- Stocks: High risk, high potential return.

- Bonds: Medium risk, moderate potential return.

- Real Estate: Medium risk, moderate potential return.

- Cash: Low risk, low potential return.

Time Horizon and Return Expectations

The length of time an investor plans to hold an investment significantly influences acceptable return rates.

Investment Strategies for Different Time Horizons

- Short-term (less than 1 year): Low-risk, liquid investments like money market accounts or high-yield savings accounts.

- Medium-term (1-5 years): A mix of bonds and stocks, balancing risk and return.

- Long-term (5+ years): Primarily stocks, allowing for greater potential growth through compounding.

Impact of Compounding

Compounding allows investment returns to generate further returns over time. This effect is magnified over longer periods.

An investment of $10,000 earning 7% annually will grow to approximately $19,671.51 after 10 years. The power of compounding is evident here as the investment grows exponentially over time.

Benchmarking Investment Performance

Comparing investment performance against relevant benchmarks provides a context for evaluating success.

Suitable Benchmarks, What is a good rate of return on investments

Benchmarks vary based on the asset class and investment strategy. Common benchmarks include the S&P 500 for large-cap US stocks, the Barclays Aggregate Bond Index for US investment-grade bonds, and specific sector indices.

Comparing Investment Performance

| Investment | Return | Benchmark | Benchmark Return |

|---|---|---|---|

| Mutual Fund A | 12% | S&P 500 | 10% |

| Bond Portfolio B | 5% | Barclays Aggregate | 4% |

Considering Fees and Taxes: What Is A Good Rate Of Return On Investments

Investment fees and taxes significantly reduce overall returns. It’s crucial to factor these expenses into return calculations.

Types of Investment Fees

- Management fees (mutual funds, ETFs)

- Brokerage fees (trading commissions)

- Expense ratios (mutual funds, ETFs)

Tax Implications

Investment income (dividends, interest) and capital gains are subject to taxes, reducing the net return. Tax rates vary depending on the investor’s income bracket and the type of investment.

Suppose an investment generates a 10% return before fees and taxes. If the management fee is 1%, the brokerage fee is 0.5%, and the capital gains tax is 15%, the net return would be approximately 7.35% (10% – 1% – 0.5% – 15% of (10%-1%-0.5%)).

Diversification and its Effect on Returns

Diversification reduces risk by spreading investments across different asset classes.

Diversified Portfolios

A well-diversified portfolio may include a mix of stocks, bonds, real estate, and other asset classes. The specific allocation depends on the investor’s risk tolerance and financial goals.

Diversification and Volatility

Diversification reduces the volatility of portfolio returns, meaning that the portfolio is less likely to experience extreme ups and downs.

Imagine two portfolios: one invested entirely in stocks and another diversified across stocks and bonds. During a market downturn, the diversified portfolio will likely experience less significant losses than the portfolio solely invested in stocks.

{kind=link}